Multi Layered Plastic Recycling: opportunities and challenges

Multi layered plastics (MLP) such as potato wafer packet, chocolate wrapper, wrappers for ready to eat foods and pharma products are criticised for their lack of recyclability, leading to littering of our cities and oceans. However, MLPs remain the cheapest and most viable option for packaging of food and pharma products and it may not be possible to completely replace them atleast in the near term. In this blog, we examine entrepreneurial opportunities available in MLP waste management and challenges faced by these businesses.

How big is the MLP waste problem?

India consumes close to 15000[efn_note]Challenges and opportunities: Plastic Waste Management in India by TERI[/efn_note] tonnes of plastics per day, of which only 60% is recycled. Packaging plastics (MLPs and single use plastics such as light weight plastic bags, coffee cups, disposable utensils), contribute to majority of the non-recycled plastics. MLPs cannot be recycled economically, as these are made of two or more layers of plastics and separating the layers is not cost effective.

MLP waste can be broadly divided into two categories: industrial waste and post use waste. Industrial waste refers to the waste generated in the flexible packaging /converting units, this waste is relatively clean and can be converted into products such as plastic ropes/bags or fuel. Post use waste comprises waste generated from households and other consumption centres such as malls, commercial establishments. Such MLPs are contaminated and have high moisture content as they are mixed with the organic waste; it is this waste, which mostly finds its way to the landfill.

Is there a shortage of MLP waste processing capacity?

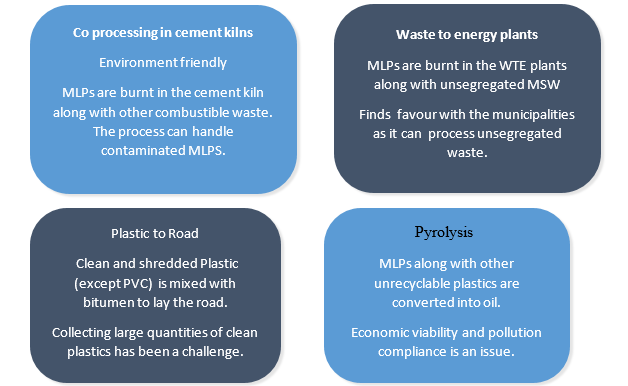

MLP waste can typically be converted into power or fuel, through a number of processes (see picture 1). Additionally, it can also be used a filler for laying roads.

Picture 1: Laminate waste treatment options

Among above mentioned methods, co processing in cement plants has taken off to an extent. Currently around 54[efn_note]Guidelines for Co processing of plastic waste in cement kilns, a report by CPCB, May 2017[/efn_note] cement plants all over the country have made investments in co processing facilities that allows them to use alternate fuel in the kiln. As per Cement Manufacturers Association (CMA), cement plants currently have a Thermal Substitution Rate (TSR) of 4%, indicating that they meet 4 per cent of their fuel requirements from alternate fuels including plastic waste. Cement industry has proposed to increase their TSR to 25% by 2025, which will allow them to consume up to 12 million tonnes of plastic waste. While cement plants can handle contaminated waste, it has to be moisture free as wet waste is difficult to process.

Waste To Energy (WTE) plants burn unsegregated waste to produce power. Currently there are around 7 operational WTE plant, 40[efn_note] Garbage management: Is waste to feasibility an option, Financial express, February 2019[/efn_note] under different stages of construction. WTE plants are ideally meant for processing dry waste, as wet waste (largely organic in nature) has lower calorific value and therefore is ineffective. However, given the lack of availability of segregated waste, they use mixed waste. While these plants have faced issues related to their compliance with pollution control norms, they are still preferred by the municipalities around the country as they can handle large amounts of unsegregated waste.

Pyrolysis refers to the process of converting plastic to oil, which can be used as a fuel. This process also needs clean /moisture free waste. Pyrolysis is yet to take off, largely to due unavailability of clean waste and risks related to the pollution compliance of such units. However, these plans can work well in industrial estates where availability of 2-3 tonnes of clean waste per day is assured.

Plastic has been used to build roads in Chennai, Indore, Pune and Meghalaya. The challenges again are lack of availability of required amount of clean plastic waste.

As such, the key issue that hampers laminate waste management is lack of availability of clean laminates that are fit to be processed and not shortage of waste processing facilities as such. The existing capacity of the cement and waste to energy facilities is enough to meet the needs of the industry.

Where are the opportunities for new businesses?

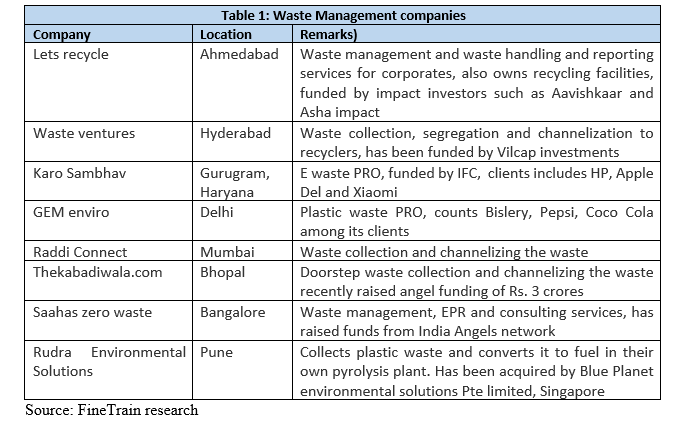

On the one hand, there is huge amount of MLP and plastic waste which needs recycling and on the other hand waste treatment providers such as cement kilns, WTE, and pyrolysis plants don’t get desired quality of waste. Thus, there is a large opportunity to set up businesses that can incentivize households to segregate dry and wet waste, collect the segregated waste and channelize it to recyclers. Given the potential opportunity, a number of companies (see Table 1) have started aggregating household waste and supplying it to recyclers.

Further, changing regulatory landscape in plastic waste management sector has boosted the viability of this sector. The regulations on plastic waste management are evolving and EPR (extended producer responsibility) was introduced in 2016. EPR makes producers, importers and brand owners responsible for processing of end of life plastic waste generated by their products. These companies can also take services of a Producer Responsibility Organisation (PRO) to manage their waste. Although, EPR for plastic waste is still in its early days, some FMCG companies have started warming up to this idea. For example, Indian Pollution Control Association (IPCA), a Delhi based PRO is implementing a project called “We Care” on behalf of FMCG companies such as PepsiCo , Nestle, Dabur and other to collect MLPS and channelize them to the recyclers. Recognition and acceptance of a PRO in plastic waste management provides a sustainable source of revenue for waste management companies and therefore makes their operations more viable.

Regulation is also slowly making an impact on waste segregation mindset of Indians. For example, in Mumbai and /Bangalore in situ (on site) composting is mandatory for bulk generators who generate more than 100 kg of waste every day as the municipality does not collect wet waste from such bulk generators.

Increasing awareness about consequences of informal recycling on the health of workers and environment is also bringing about a change in the mindset of people to own up their waste and sell it only to authorised recyclers. This in turn is likely to lead to an increase in demand for PROs in the long term.

What are the key challenges?

While the opportunity is large, the waste management companies face challenges related to lack of adequate clean waste and funding.

- Competition from informal sector: Almost all companies in formal waste recycling sector including e waste, bio-waste and plastic waste do not get adequate waste. For example more than 90 per cent of[efn_note]Managing India’s electronic waste, Live Mint, May 2017[/efn_note] e waste is handled by informal sector and 50 per cent[efn_note]Report on Indian Plastics Industry by Plastindia Foundation, Jan 2018[/efn_note]of plastic recycling is done by informal sector, resulting in less than adequate availability of waste to the formal recyclers. The informal sector is able to offer higher prices for the waste vis a vis formal recyclers as they their processing costs are lower due to lower operational/manpower costs/capex costs. For example, a formal plastic recycling units needs to invest at at-least Rs. 1 cr in a recycling unit including the processing machinery and pollution control equipment for treating dust and waste water. However, the cost for informal sector are negligible as most of the work is done manually, and without any compliance to pollution control.

- Access to funding: The waste related business are working capital intensive, as they need to pay for the waste upfront, while they get paid only after sizable quantity of each type waste is collected, sorted and sent to the recycler. Additionally, they need large godown for waste storage and employ a number of people in sorting the waste. Further, they require funds for conducting awareness campaigns and marketing. Since these businesses do not have large physical assets, traditional channels such as bank are not able to meet their requirements. Similarly, such businesses also find it difficult to attract equity capital, as it is difficult to scale up operations across geographies.

However, emergence of impact investors and green funds has improved the funding prospects of these businesses. As can be seen in the Table 1, a number of investors including IFC, Aavishkaar, Asha impact and angle investors have invested in waste related businesses.

How can we help?

We are an advisory firm for small and medium enterprises in green industries. We can help you assess viability of your proposed plastic waste related venture including availability of waste, technology selection and market for recycled products. If you already have a waste related business, we can support you in raising capital for your growth plans and also in acquiring green businesses.

Reach us @

Write to us: bchhatre@finetrain.com, admin@finetrain.com

Call us: +91 800 888 4932